INVESTMENT PRODUCTS

DST/1031 Exchange Solutions

The Process

How a 1031 Exchange into a DST Works

Sell Your Property

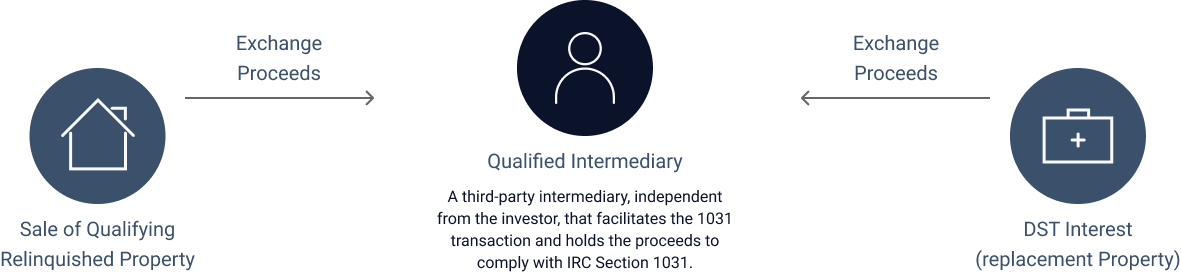

An investor sells their investment real estate and engages a Qualified Intermediary to hold the proceeds during the exchange period.

Identify Replacement Property

Within 45 days, the investor identifies up to three qualifying like-kind replacement properties, which may include DST interests.

Select a DST

The investor selects a DST offering that meets their exchange requirements, acquiring a fractional interest in an institutional real estate asset.

Close Within 180 Days

The exchange is completed when the Qualified Intermediary transfers proceeds to acquire the DST interest, deferring capital gains taxes.

UNDERSTANDING THE BASICS

What is a 1031 Exchange?

A 1031 exchange — named for Section 1031 of the U.S. Internal Revenue Code — allows real estate investors to defer capital gains taxes when selling an investment property, provided the proceeds are reinvested into a qualifying “like-kind” replacement property within specific timeframes.

To qualify, investors must identify a replacement property within 45 days of selling their original property, and must complete the purchase within 180 days. When structured correctly, a 1031 exchange can be a powerful tool for preserving equity and compounding wealth across multiple real estate transactions.

THE DST STRUCTURE

What is a Delaware Statutory Trust?

A Delaware Statutory Trust (DST) is a legally recognized trust structure that allows multiple investors to hold fractional ownership interests in institutional-grade real estate. The IRS has ruled that DST ownership interests qualify as “like-kind” property for 1031 exchange purposes.

Because a DST is professionally managed, investors participate in real estate ownership without taking on the responsibilities of direct property management. Each investor holds a beneficial interest in the trust, proportional to their investment, and the trust owns the underlying real estate asset.

DSTs are commonly used by investors completing 1031 exchanges who want access to larger, institutional-quality assets that may be difficult to acquire individually.

THE PROCESS

How a 1031 Exchange Works

A 1031 exchange allows an investor to sell an investment property and reinvest the proceeds into another qualifying “like-kind” real estate asset, deferring recognition of capital gains taxes

45 Days

Identification Period

Investor must identify up to three qualifying like-kind replacement properties within 45 days of the sale closing.

180 Days

Exchange Period

The full exchange -- including closing on the replacement property -- must be completed within 180 days of the original sale.

Key Features

- Property must be “like-kind”, i.e. real property held for investment, which includes retail, office, residential income, mineral rights, etc.

- Property must be “like-kind”, i.e. real property held for investment, which includes retail, office, residential income, mineral rights, etc.

- Proceeds must go through a qualified intermediary (QI) (or directly from sale escrow with appropriate documentation)

- Debt and equity must be fully replaced to avoid “boot”

General Investor Experience

- Engage QI prior to sale

- Sell relinquished property to a buyer through QI

- Complete paperwork to purchase DST interest

- Apply for customizable loan program, if applicable

- Close on the purchase of DST interest

- Defer taxes, with tax basis carried over to DST interest

STRUCTURE OPTIONS

TIC and DST Structures

Two 1031-eligible ownership structures, each suited to different investor objectives. Understanding the differences can help determine which format best aligns with your exchange goals.

TENANCY IN COMMON

TIC Structure

Direct co-ownership interest in real estate — typically fewer investors per asset with greater customization.

DELAWARE STATUTORY TRUST

DST Structure

Passive beneficial interest in a trust that holds institutional real estate — designed for streamlined execution and flexible sizing.

WHAT IT IS

Direct tenancy-in-common ownership in real estate (1031 eligible). Each investor holds a deeded fractional interest in the property and participates in major decisions, offering more control and flexibility over the investment.

Passive beneficial interests in a Delaware Statutory Trust that owns real estate (1031 eligible). Investors hold an interest in the trust — not the property directly — allowing for streamlined administration and flexible investment sizing.

BEST FIT FOR

- Investors seeking growth-oriented or value-add strategies.

- Investors willing to participate in major decisions and hold for longer periods.

- Larger allocations requiring customized ownership objectives.

- Investors prioritizing simplicity and passive ownership

- Investors who want institutional execution without day-to-day involvement

- 1031 investors with timing constraints who value smoother closing mechanics

PRIMARY BENEFITS

- Tailored structuring for more sophisticated investor needs

- Supports larger allocations and customized ownership objectives

- Better suited for flexible strategies, including value-add, subject to deal terms

- Lower minimums can allow diversification across multiple offerings

- Fully passive ownership with standardized administration and reporting

- Designed for efficient 1031 exchange within required timelines

TRADE-OFFS

- Larger minimum investment amount

- Investor approval typically required for major changes to business plan

- Less flexibility to modify structure post-close

- Exit is governed by the terms of the offering

WHY IT MATTERS

Investors can leverage exchanges to defer taxes, which may help them retain their investable proceeds and increase their purchasing power

15-20%

Federal tax rate

≤ 25%

Federal depreciation recapture tax rate

≤ 13.3%

State tax rate

3.8%

Net investment income tax

Total Taxes on Sale of Property Can Exceed 37% - Potential Tax Savings of a 1031 Exchange

$581,500

~25% Difference in Investable Proceeds

For illustrative purposes only. Figures are hypothetical and do not represent actual results.

HYPOTHETICAL ILLUSTRATION

Difference in Net Investable Proceeds: Taxable Sale vs. Tax-Deferred 1031 Exchange

Sell Property & Pay Taxes

Complete 1031 Exchange & Defer Taxes

PROPERTY BASIS

Purchase Price

$1,000,000

$1,000,000

Depreciation

$500,000

$500,000

Loan Balance**

$300,000

$300,000

Adjusted Cost Basis

$500,000

$500,000

SALE

Sale Price

$2,000,000

$2,000,000

Total Taxable Gain

$1,500,000

$1,500,000

TAXES

Depreciation Recapture Tax (25%)

$125,000

—

Federal Long-Term Capital Gains Liability (20%)

$200,000

—

State Tax (13.3%)

$199,000

—

Net Investment Income Tax (3.8%)

$57,000

—

Total Taxes Due

$581,500

—

Net Proceeds for Investment

$1,418,500

$2,000,000

For illustrative purposes only. Figures are hypothetical and do not represent actual tax or investment advice. State tax rate shown reflects California maximum rate. Consult your tax advisor for guidance specific to your situation.